|

ГЛАВНАЯ

> Вернуться к содержанию

SENTENTIA. European Journal of Humanities and Social Sciences

Правильная ссылка на статью:

Zhao W.

The measurement and dynamics of financial openness of Chinese economy

// SENTENTIA. European Journal of Humanities and Social Sciences.

2022. № 3.

С. 1-13.

DOI: 10.25136/1339-3057.2022.3.37774 EDN: GHTZCA URL: https://nbpublish.com/library_read_article.php?id=37774

The measurement and dynamics of financial openness of Chinese economy /

Уровень и динамика финансовой открытости китайской экономики

Zhao Weili

ORCID: 0000-0002-3983-9490

аспирант, экономический факультет, Южный федеральный университет

344006, Россия, Ростовская область, г. Ростов-На-Дону, ул. Большая Садовая, 105

Zhao Weili

Postgraduate student, Faculty of Economics, Southern Federal University

344006, Russia, Rostovskaya oblast', g. Rostov-Na-Donu, ul. Bol'shaya Sadovaya, 105

|

1193721568@qq.com

|

|

|

Другие публикации этого автора

|

|

|

DOI: 10.25136/1339-3057.2022.3.37774

EDN: GHTZCA

Дата направления статьи в редакцию:

01-04-2022

Дата публикации:

07-11-2022

Аннотация:

В настоящее время существует множество публикаций, посвященных изучению связи между финансовой открытостью и другими экономическими характеристиками стран с развивающейся экономикой. При этом точность измерения финансовой открытости является предпосылкой оценки ее эффектов. Разные ученые формируют разные индикаторы, отражающие различные аспекты финансовой открытости, что приводит к систематически отличающимся результатам анализа. Следовательно, необходимо построить комплексный показатель и всесторонне измерить финансовую открытость. Новизна данной статьи заключается в выдвинутой автором идее «облегчения финансовой открытости». В статье сформирован новый дополнительный индикатор, связанный с упрощением финансовой открытости. В отличие от предыдущих публикаций, в настоящем исследовании утверждается, что, хотя некоторые факторы не имеют прямого отношения к финансовой открытости, они могут облегчать работу финансовых институтов и поддерживать приток международного капитала, поэтому они также играют важную роль. В работе измерена финансовая открытость как с данной позиции, так и с точки зрения открытости финансовых счетов и открытости финансовых институтов. Этот совершенно новый подход может способствовать дальнейшим исследованиям при изучении связи между финансовой открытостью и состоянием национальной экономики. Кроме того, опыт Китая в области финансовой открытости может дать много полезной информации другим развивающимся странам.

Ключевые слова:

финансовая открытость, финансовый институт, развивающаяся экономика, Китай, финансовое регулирование, инвестиции, финансовый рынок, экономическая политика, институты развития, экономическая структура

Abstract: Currently there are many literatures examining the linkage between financial openness and other economic factors in emerging economies. Nevertheless, the accuracy of measurement of financial openness is the prerequisite of evaluating its effects. Different scholars usually construct different indicators that capture different facets of financial openness, hence yielding systematically different regression results. Therefore, it is necessary to construct a comprehensive indicator and measure the financial openness in an all-around way. The innovation of this paper lies in the concept of “financial opening facilitation” that is newly put forwarded by the author. This paper constructs a new sub indicator: financial opening facilitation. Different from previous literatures, this paper argues that although some factors are not directly related to financial opening, they can facilitate the operation of financial institutions and support the flow of international capital, so they also play an important role. The author measures the financial openness in terms of financial account openness, financial institutions openness, financial opening facilitation. This brand-new method can be conducive to the further researchers when they examine the relation between financial openness and domestic economy. Furthermore, China's experience of financial opening can give many revelations to other emerging countries.

Keywords: financial opening, financial institution, emerging economy, China, financial regulation, investment, financial market, economic policy, development institutions, economic structure

Introduction

Financial openness is to reflect the degree of financial opening in a certain country or region. Regarding the connotation of financial opening, there is no uniform definition in the academia. The concept of financial opening comes from the concept of financial liberalization. Initially, McKinnon thinks that the governments of developing countries generally adopt compulsory administrative methods to control interest rates, which hinders economic growth, that is so-called financial repression [1]. He advocates financial liberalization and insists the government should deregulate and let the market dominate the economic operation. With the evolution of financial liberalization theory, more concepts such as “financial globalization”, “financial integration”, “financial opening” are raised by scholars. These concepts have similar meanings and have often been used interchangeably in the literature. For instance, Hartmann et al describe Euro-Area financial integration is an integration of money markets, bond markets, equity markets, and banking [2]. Heathcote and Perri label the trend that international trade in financial assets has sharply increased and financial markets are becoming increasingly integrated internationally as financial globalization [3]. Carmignani and Chowdhury separate the concept of financial opening from financial integration and indicate that financial opening is the process of lifting administrative or legal restrictions on capital movements and hence creating the necessary conditions for the integration of the domestic financial system into the global market [4].

This paper holds that financial opening has two connotations: static connotation and dynamic connotation. In terms of static connotation, it refers to the nature state of the internationalization of local financial services, the localization of foreign financial services and the actual result of capital flow in a country. In terms of dynamic connotation, it refers to the process of a country (or region) gradually realizing the internationalization of local financial services, the localization of foreign financial services and the free flow of capital. Therefore, financial opening should include both financial accounts opening and financial institutions opening.

The accuracy of measurement is the prerequisite for accurately predicting and evaluating the effects of financial openness. Researchers have available to them numerous indicators of financial openness and integration [5]. All these indicators can be roughly divided into two broad categories: de jure, de facto, with unique advantages and disadvantage. De jury measure is more clear, because all the documents of financial regulations and policies are available publicly, they are easy to be assigned values for judgement; while it has a certain subjectivity. De facto measure reflects the extent to which actual capital flows evolve in response to legal restrictions; while it fluctuates greatly and are more volatile, and thus noisy [6].

Therefore, this paper introduces a hybrid method to measure China's financial openness. This paper argues that the internationalization level of RMB and participation in relevant leading international financial organizations can facilitate the operation of financial institutions and the flow of cross-border capital. Incorporating these factors, this paper constructs a new sub indicator: financial opening facilitation. Hence, in order to get the final time-series values of financial openness, this paper calculates three sub-indices: financial account openness, financial institutions openness, financial opening facilitation. Using Principal Component Analysis, this paper assigns these three sub indicators different weights and aggregate them in the model specification. At last, this paper analyses the dynamics of financial openness of Chinese economy.

Because the Annual Report on Exchange Arrangements and Exchange Restrictions issued by the International Monetary Fund cannot fully reflect the changes in China's financial openness, this paper mainly drown on data and materials from China's financial Yearbook, The events of China's reform and opening up: 1978-2008 , The 30 years of China's utilization of foreign capital, and the relevant statement and column in Annual report of the State Administration of foreign exchange issued by the State Administration of Foreign Exchange every year. To measure the internationalization level of RMB, this paper adopts RMB Internationalization Index compiled by Renmin University of China based on RMB Internationalization Report which is issued by The people’s bank of China. In order to keep the data consistent and taking into account the availability of the data, all the data in this study are collected from 1980-2020.

The financial account openness

In the measurement of financial account openness, de jury measures are usually based on AREAER,coding qualitative description of the sub-items in the capital transaction, items of each country. For instance, Cottarelli and Giannin set a 0/1 binary dummy variable to represent the openness level of financial account. Where, 0 indicates that the financial account is completely under control and 1 indicates that the financial account is fully open [7]. On the basis of their research, Montiel and Reinhart divided financial account control into three grades [8]. Chinn and Ito construct KAOPEN index. Using Principal Component Analysis, KAOPEN is the first standardized principle component of all variables in the function. Higher scores indicate greater openness [9]. De facto methods measure the opening level of financial account from the perspective of actual capital flow. These methods can be divided into two categories: priced-based, quantity-based. Among price-based measures, Feldstein and Horioka (1980) construct an indicator to reflect the correlation between savings and investment. They believe if the savings and investment of a country or region are equal, it will indicate that the country implements strict capital account control; while a country or region completely opens its financial account, its savings rate and investment rate will be uncorrelated.

Nevertheless, currently when scholars examine the linkage of financial openness and domestic economy, they usually measure the financial openness in terms of capital flows or stocks,with quantity-based method. It can be found in the works of Cerdeiro and Komaromi [10], Yasmeen et al [11], Ashraf et al [12], Amin et al [13]. They evaluated the effect of financial openness on industry specification, capital flow, financial development, entrepreneurship, bank loan pricing, natural resources respectively.

This paper holds that the financial account openness mainly focus on the transformation of specific financial system, the relaxation of financial regulations and policies. Compared with de facto measures, de jury measure can directly reflect the specific content of financial opening and related to a government's policy stance. But traditional de jury methods adopt dummy values only based on AREAER; it is ambiguous and not detailed enough for a case study on a specific country. On the basis of the research results of Lan [14], this paper constructs the formula of measuring financial account openness as follows:

(1) (1)

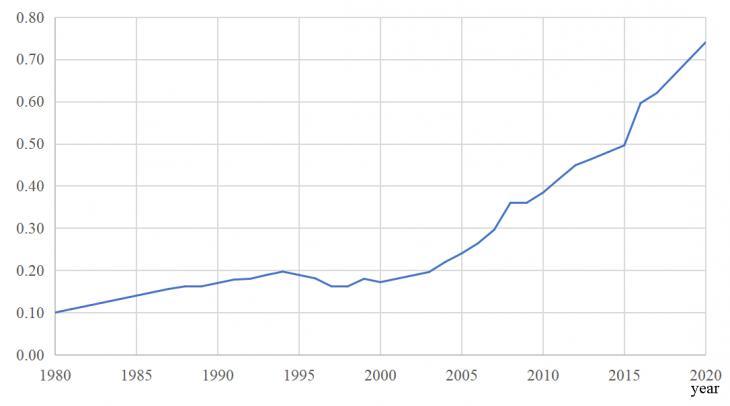

In this formula, n stands for the total number of sub items of the financial account; P (i) stands for the openness level of each sub item i. According to the classification method of the International Monetary Fund (IMF), this paper divides the financial account into 7 categories, 11 items and 40 sub items, and divides the openness of each sub item into four grades and assigns them value respectively: non-convertible (0), partially convertible (1/3), basically convertible (2/3) and fully convertible (1). According to the AREAER in 2011, there were 4 nonconvertible sub items in China, accounting for 10%; 22 partially convertible sub items, accounting for 55%; 14 basically convertible sub items, accounting for 35%. According to the above formula, the openness level of China's financial account in 2011 is: (4*0+22*1/3+14*2/3+0*1)/40=0.417. This shows that China's financial account openness was at a medium level in 2011. Taking 2011 as the base period, this paper speculates the financial account openness level in China backward from 1980 to 2010 and forward from 2012 to 2020. For instance, if the restriction degree of one sub item is relaxed compared with the previous year, it will be added by 1/3; If it is tightened compared with the previous year, it will be reduced by 1/3; If there is no change, neither added nor reduced. The annual financial account openness index is the annual change divided by 40 plus the score of the previous year. In this way, this paper obtains the time-series values of China's financial account openness from 1980 to 2020 (Figure 1).

Figure 1: The annual index of financial account openness from 1980 - 2019

Source: compiled by the author according to the research data.

The Financial institutions openness

From history, although it is rare, there are some scholars measure the financial openness in terms of financial institutions. For instance, Claessens and Glaessner examined the openness of financial service sectors (including banking, insurance and securities) from the perspective of market access [15]. Based on their research, Mattoo distinguishes different modes of financial services, and makes a quantitative study on the barriers in financial services of developing countries and economies in transition, then constructs the liberalization index which is the weighted average of the value of the most restrictive measure applied by a country to each mode in the sector [16]. Luo et al employ financial Freedom Index (FINFREE) and the percentage of foreign-owned banks operating in the domestic market (FOREIGN) to measure the extent of government intervention in banks and other financial institutions [17].

On the basis previous researches, this paper goes further and measures the openness level of the three sectors (banking, insurance and securities) respectively in terms of both market access and national treatment. Articles XVI and XVII are found in GATS Part III entitled ‘Specific Commitments’. Commitments are specific because each Member may choose to what extent the obligations contained in these provisions are applicable to them.

1. Market access.

Market access refers to the degree to which a country allows foreign financial institutions and enterprises to enter the domestic financial market. According to Article XVI, each Member shall accord to services and service suppliers of any other Member treatment no less favorable than that provided for under the terms, limitations and conditions agreed and specified in its Schedule. Article XVI:2 contains a list of measures that Members shall not maintain in sectors where full market access commitments are undertaken. These are: (a) limitations on the number of suppliers; (b) limitations on the total value of service transactions or assets; (c) limitations on the total number of service operations or on the total quantity of service output; (d) limitations on the total number of natural persons that may be employed; (e) measures which restrict or require specific types of legal entity or joint venture; and (f) limitations on the participation of foreign capital [18].

According to the opening process of China's financial service industry, this paper sets the following principles and assigns different values of the market access for banking, insurance and securities sectors respectively (Table 1).

Table 1: The assigned values in market access.

Source: compiled by the author according to the research data.

|

Assigned values

|

Banking sector

|

Security sector

|

Insurance sector

|

|

0

|

The market is completely closed

|

The market is completely closed

|

The market is completely closed

|

|

1/6

|

Allow foreign banks to set up representative establishments in specific areas on permission

|

Allow foreign securities institutions to set up representative establishments in specific areas on permission

|

Allow foreign insurance companies to set up representative establishments in specific areas on permission

|

|

2/6

|

Allow foreign institutions to set up banks in specific areas on permission

|

Allow foreign institutions to set up joint venture securities company in specific areas on permission

|

Allow foreign institutions to set up insurance companies in specific areas on permission

|

|

3/6

|

Allow foreign institutions to set up banks in China on permission

|

Allow foreign institutions to set up joint venture securities company in China on permission

|

Allow foreign institutions to set up insurance companies in China on permission

|

|

4/6

|

Relax the restrictions on the proportion of foreign shares in banks

|

Relax the restrictions on the proportion of foreign shares in securities companies

|

Relax the restrictions on the proportion of foreign shares in insurance companies

|

|

5/6

|

Management model with a negative list

|

Management model with a negative list

|

Management model with a negative list

|

|

1

|

No control

|

No control

|

No control

|

2. National treatment.

Unlike Article XVI, Article XVII in GATS does not set out a list of prohibited measures. Instead, it indicates a member should accord to services and service suppliers of any other Member, in respect of all measures affecting the supply of services, treatment no less favorable than that it accords to its own like services and service suppliers [19]. Formally identical or formally different treatment shall be considered to be less favorable if it modifies the conditions of competition in favor of services or service suppliers of the Member compared to like services or service suppliers of any other Member.

This paper also assigns the value of the national treatment for banking, insurance and securities sectors respectively (Table 2).

Table 2: The assigned values in national treatment.

Source: compiled by the author according to the research data.

|

Assigned values

|

Banking sector

|

Security sector

|

Insurance sector

|

|

0

|

No business

|

No business

|

No business

|

|

1/5

|

Nonprofit business

|

Nonprofit business

|

Nonprofit business

|

|

2/5

|

Some profitable business in specific areas on permission

|

Some profitable business in specific areas on permission

|

Some profitable business in specific areas on permission

|

|

3/5

|

Profitable business in china on permission

|

Profitable business in china on permission

|

Profitable business in china on permission

|

|

4/5

|

Further deregulation of business scope

|

Further deregulation of business scope

|

Further deregulation of business scope

|

|

1

|

National treatment

|

National treatment

|

National treatment

|

According to the above evaluation system, firstly this paper establishes the measurement formula of the openness level of each financial sector:

(2) (2)

In this formula, is the openness level of financial sector i (including banking, insurance and securities) in a certain period t; and respectively indicate the openness level of financial sector i in terms of market access and national treatment in period t; andare the weights corresponding to the above two variables. This paper regards Market Access is in the same position with Nation treatment for an openness level of a financial sector. This paper gives the same weight (0.5) to market access and national treatment.

Then, the measurement formula of a country's overall financial institutions openness can be presented as follow:

(3) (3)

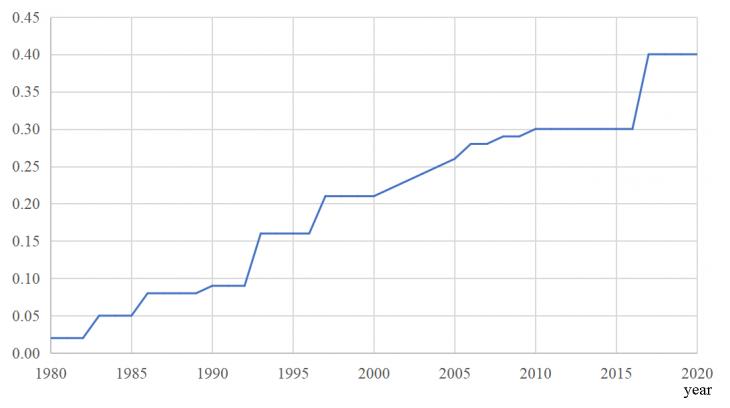

In this formula, FO2t is the overall openness level of China's financial institutions in period t;, FOBt, FOIt , FOst respectively represent the openness level of China's banking, insurance and securities sectors in period t; WB, WI, and Ws are the weights corresponding to the above three variables. This paper gives the same weight (1/3) to the three sectors. The result is presented in Figure 2.

Figure 2: The annual index of financial institutions openness from 1980- 2020

Source: compiled by the author according to the research data.

Financial opening facilitation

The financial opening facilitation is to reflect the relevant financial support factors for the opening of financial account and financial institutions. They mainly include the amount of international financial organizations China has participated in and internationalization level of RMB. The more international financial organizations China has joined in and the higher RMB internationalization level will be more conducive to international financial transaction, internationalization of domestic financial institutions and localization of foreign institutions. Since reform and opening up, China has gradually joined international financial organizations (Table 3). The internationalization process of a currency will generally go through the stages of settlement, foreign exchange transaction, national reserve. In 2009, the People's Bank of China successively announced the "Administrative Measures for the Pilot RMB Settlement of Cross-border Trade" and its "Detailed Implementation Rules". So, 2009 is regarded as the very beginning point of RMB internationalization. To reflect the level of RMB internationalization, this paper adopts RMB internationalization index compiled by Renmin University of China. It is constructed as follows.

(4) (4)

Among them, RIIt stands for the RMB internationalization index in period t, Xjt stands for the value of the J variable in period t. Wjis the weight of the J variable. The economic meaning of RII should be interpreted as follows: If the RMB is the only international currency in the world, the value of each variable in the RII index should be equal to 100%, and RII is 100 at this point. Conversely, if the RMB is not used at all in any international economic transactions, the value of each variable is equal to zero, and RII is zero too. If the value of RII keeps increasing, it indicates that its internationalization level is getting higher and higher. For example, when the RII is 10, it means that in the international trade transaction, capital flow, and official foreign exchange reserve asset of all the countries across the world, RMB account for one-tenth share [20]. The point of note here is that because the initial RMB international index is in a scale from 1-100, for the consistency of the value, it should be rescaled from 0-1. The overall financial opening facilitation index is constructed as follow.

(5) (5)

In this formula, is the financial opening facilitation Index, RIIt represents the newly scaled RMB internationalization index in period t; at represents the amount of international financial organizations China has participated in period t ; are set as the weight of each variable. This paper holds that the above two variables are in the same weight, so they are given the same weight (0.5). Because 2009 is regarded as the very beginning point of RMB internationalization,so the value of RMB internationalization index before 2009 is regarded as zero. The annual index of financial opening facilitation from 1980-2020 is presented in figure 3.

Table 3: International financial organizations China has joined in since reform and opening up

Source: compiled by the author according to the research data.

|

International financial organizations (IFO)

|

Assigned values

|

|

International bank

|

Not joined 0

|

|

Joined 1

|

|

International monetary fund

|

Not joined0. 0

|

|

Joined 1

|

|

International development association

|

Not joined. 0

|

|

Joined 1

|

|

Society for Worldwide Interbank Financial Telecommunications(swift)

|

Not joined. 0

|

|

Joined 1

|

|

General agreement on Tariffs and trade

|

Not joined 0

|

|

Joined 1

|

|

Asian development bank

|

Not joined 0

|

|

Joined 1

|

|

Multinational Investment Guarantee Agency

|

Not joined 0

|

|

Joined 1

|

|

Bank for International Settlements

|

Bot joined 0

|

|

Joined 1

|

|

International Chamber of Commerce

|

Not joined. 0

|

|

Joined 1

|

|

International organization of Securities Commissions

|

Not joined. 0

|

|

Joined 1

|

|

International Association of insurance regulators

|

Bot joined. 0

|

|

Joined 1

|

|

World Trade Organization

|

Not joined 0

|

|

Joined 1

|

|

International Finance Corporation

|

Not joined. 0

|

|

Joined 1

|

Figure 3: The annual index of financial opening facilitation from 1980-2020

Source: compiled by the author according to the research data.

The overall financial openness

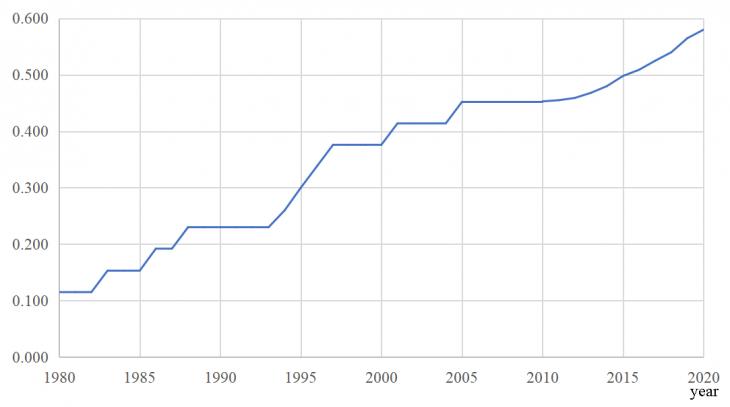

Based on the financial account openness and financial institution openness, financial opening facilitation we calculated above, this paper constructs a comprehensive index to measure China's financial openness by giving certain weights to these three sub-indices respectively. Principal Component Analysis is a common method to reduce the dimension of multiple indicators and then combine them into a new comprehensive index [21]. This paper uses SPSS software and Principal Component Analysis to give weight to each sub index. Principal Component Analysis is divided into three steps: 1. Constructing principal component sequence and extracting principal components according to the standard with eigenvalue greater than 1; 2. The component matrix is obtained by calculating the eigenvector corresponding to the eigenvalue and standardizing it; 3. Calculate the weight of each sub index in the principal component. The analysis results are shown in Table 4. The results show that the eigenvalue of the first principal component is 2.76, which explains 91.989% of the total variance. So, its components are proposed to determine the index weight.

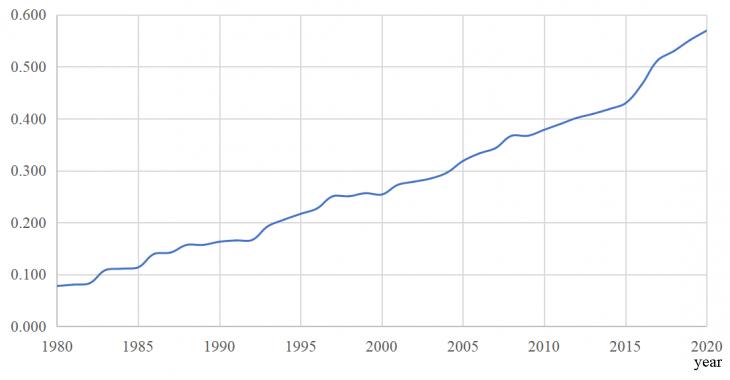

In the component matrix, the eigenvector corresponding to the eigenvalue in the first principal component is (0.333, 0.357, 0.351). Then, divide them by the square root of the corresponding eigenvalue to obtain the weight of each sub indicator. The formula 6 is the final model specification for the comprehensive index of China's financial openness. The time-series value of overall financial openness is presented in figure 4.

(6) (6)

Table 4: The result of Principle Component Analysis

Source: compiled by the author according to the research data.

|

Component Initial Eigenvalues Extract the sum of squares of the loads

|

|

Eigenvalue

|

Variance Proportion

|

Accumulation

|

Eigenvalue

|

Variance Proportion

|

Accumulation

|

|

1) 2.76

|

91.989

|

91.989

|

2.76

|

91.989

|

91.989

|

|

2) 0.226

|

7.525

|

99.513

|

|

|

|

|

3) 0.015

|

0.487

|

100

|

|

|

|

|

Component matrix

|

|

Financial account openness

|

Financial institutions openness

|

Financial opening facilitation

|

|

0.333.

|

0.357

|

0.351

|

|

Principal component score

|

|

Financial account openness

|

Financial institutions openness

|

Financial opening facilitation

|

|

0.200

|

0.215

|

0.211

|

| |

|

|

|

|

|

|

|

|

|

Figure 4: The annual financial openness index in China from 1980-2020

Source: compiled by the author according to the research data.

The dynamics of financial openness of Chinese economy

Generally speaking, from the perspective of time-series analysis, China’s financial opening process has gone through the following stages:The first stage is from 1978 to 1991, which is the stage of transformation from planned economy to market economy. The practice of financial opening at this stage mainly focused on two aspects. One is to establish special economic zones, which implement special policies such as permitting foreign financial institutions set up representative establishments. Another is to relax the control on the financial account so as to introduce foreign capital and advanced technology to support the development of domestic economy.

The second stage is from 1992 to 2000. During this period,foreign financial institutions are allowed to set up branches to engage in profitable financial businesses on permission. China also joined in the leading financial international organizations, such as Bank for International Settlements,International organization of Securities Commissions,International Association of insurance regulators .The foreign exchange system reform in 1994 is the most important reform of China's foreign exchange system. Its core content is to change from the fixed exchange rate system to a managed floating exchange rate system. In 1996, RMB was freely convertible under the current account.

The third stage is from 2000 to 2008. Some major events at this stage have promoted the great leap of China's financial openness. First of all, when China joined the WTO in 2001, it promised to open the financial service sector to the outside world within five years. From 2001 to 2008, with the super rapid development of China's economy, China's foreign exchange reserves soared a lot. In order to alleviate the pressure of domestic inflation, China began to encourage enterprises to invest abroad. In July 2005, China carried out another important reform of the foreign exchange system, giving up the peg to the US dollar and beginning the peg to a basket of currencies.

The fourth stage is from 2009 to now. The outbreak of the financial crisis in 2008 and quantitative easing policies by the Federal Reserve created an excellent opportunity for the RMB internationalization. With the announcement of "Administrative Measures for the Pilot RMB Settlement of Cross-border Trade", RMB internationalization officially started in 2009. In 2018, General Secretary Xi announced at the Boao Forum of Asia that financial opening is the primary task of China's opening up to the outside world. Since then China began to implement negative list management model and national treatment for foreign institutions.

In the past 40 years, the logic of China's financial opening is clear. From a macro perspective, China's financial opening has the following characteristics. First, the evolution and deepen of financial openness is based on the needs of real economy. Financial opening is to serve the development of the real economy, it is mainly reflected in financial account openness. Secondly, China adopts a gradual and discreet financial opening policy, selecting pilot zones first and then promoting across the country, it is mainly reflected in financial institutions openness. Third, China's financial opening process has been stable. In the process of financial opening in developing countries, there are many financial crises. China is the only country which has maintained rapid economic growth for more than 40 years and has not experienced a global or systemic financial crisis. It is inseparable from the help from relevant international financial organizations and the influence of gradually increasing RMB internationalization level. After the outbreak of COVID-19, the global economy was seriously affected. China has become one of the few countries with GDP positive growth because of effective control of the pandemic. Therefore, capital inflow into China has strong driving-force. So far, there have been almost no obstacles to capital inflow into China, but the outflow is still strictly controlled. The next step in financial opening should focus on allowing more capital outflows. On September 10, 2021, Guangdong, Hong Kong and Macao District officially launched "cross border financial link", allowing local residents to invest in financial products issued in Hong Kong. In the context of strict control of real estate in the mainland, residents need more investment channels. So, cross-border financial management will be a key step in deepening China’s financial openness.

Conclusion

This article introduces a brand-new method to measure the financial openness. Different from previous literatures, taking into account the actual factors, which are not directly related to financial opening, but can facilitate the operation of financial institutions and support the flow of cross-border capital, this paper constructs a new sub indicator: financial opening facilitation. Therefore, this paper measures the financial openness in terms of financial account openness, financial institutions openness, financial opening facilitation. The financial openness indicator in this paper is a hybrid indicator in the sense that this paper adopts de jury method to measure the openness level of financial account and financial institutions and de facto method to measure the degree of financial opening facilitation. This paper makes a time-series analysis of China’s financial opening process based on a principal components model. It indicates that China’s financial opening is discrete and prudent. The financial opening process is stable. It is to serve the development of real economy. From history, China has maintained rapid economic growth for more than 40 years without financial crisis. Therefore, China's experience of financial opening can give many revelations to other emerging countries. Furthermore, this brand-new method measures the financial openness in an all-around way, it can be conducive to the further research on the relation between financial openness and domestic economy.

Библиография

1. Yasmeen H., Tan Q., Zameer H. Discovering the relationship between natural resources, energy consumption, gross capital formation with economic growth: can lower financial openness change the curse into blessing // Resources Policy. 2021. №71(5). Pp.102013.

2. Cerdeiro D.A., Komaromi A. Financial openness and capital inflows to emerging markets: in search of robust evidence // International Review of Economics & Finance. 2021. №73(2).

3. Chinn M.D., Ito H. What matters for financial development? Capital controls, institutions, and interactions? // Journal of Development Economics. 2006. №81(1). Pp.163-192.

4. Montiel P., Reinhart C.M. Do capital controls and macroeconomic policies influence the volume and composition of capital flows? evidence from the 1990s // Journal of International Money & Finance. 1999. №18. Pp. 619-635.

5. Cottarelli, C., Giannini, C. Credibility Without Rules? Monetary Frameworks in the Post-Breton Woods Era // IMF, Occasional Paper.-1997.-№154.

6. Lane P.R., Milesi-Ferretti G.M. The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970-2004 // IMF Working Paper. 2006. № 06/69.

7. Quinn D., Schindler M., Toyoda A.M. Assessing measures of financial openness and integration // IMF Economic Review. 2011. № 59(3). Pp. 488-522.

8. Heathcote J., Perri F. Financial globalization and real regionalization // Journal of Economic Theory. 2004. № 119 (1). Pp. 207-243.

9. Carmignani F., Chowdhury A. The impact of financial openness on economic integration: evidence from the Europe and the Cis // Economics Faculty Research and Publications. 2006. №73. DOI: 10.1007/3-540-34264-8_11.

10. Rostow W.W., McKinnon R.I. Money and Capital in Economic Development // American Political Science Review. 1974. №68(4). Pp.1822.

11. Hartmann P., Maddaloni A., Manganelli S. The euro-area financial system: structure, integration, and policy initiatives // Oxford Review of Economic Policy. 2003. №19(1). Pp.180-213.

12. Ashraf B. N., Qian N., Shen Y.V. The impact of trade and financial openness on bank loan pricing: evidence from emerging economies // Emerging Markets Review. 2021. №47. Pp.100793.

13. Cerdeiro D.A., Komaromi A. Financial openness and capital inflows to emerging markets: in search of robust evidence//International Review of Economics & Finance. 2021. № 73(2).

14. Lan Faqin. Measurement of China's capital account opening // Journal of East China Normal University (SOCIAL SCIENCE EDITION). 2005. №37 (2). Pp. 87-94 (In Chinese).

15. Claessens, S., Glaessner, T. Internationalization of financial services in Asia // Social Science Electronic Publishing, 1998. DOI:10.1109/PIMRC.2006.254154

16. Mattoo A. Financial services and the WTO: Liberalization commitments of the developing and transition economies // The World Economy. 1999. №23(3). Pp. 351-386.

17. Luo, Y., Tanna, S., Vita, G.D. Financial openness, risk and bank efficiency: cross-country evidence // Journal of Financial Stability. 2016. Pp. 132-148.

18. Muller G. Troubled Relationships under the GATS: Tensions between Market Access (Article XVI), National Treatment (Article XVII), and Domestic Regulation (Article VI) // World Trade Review. 2017. №16(3). Pp. 449–474.

19. Wang W. On the Relationship Between Market Access and National Treatment Under the GATS // International Lawyer. 2012. №1045.

20. Tu Yonghong. RII--a new indicator to measure the real level of RMB internationalization // International Monetary Review. 2013 (In Chinese).

21. Jolliffe I.T., Cadima J. Principal component analysis: a review and recent developments // Philosophical Transactions of the Royal Society Mathematical Physical & Engineering Sciences. 2016.

References

1. Yasmeen H., Tan Q., Zameer H. Discovering the relationship between natural resources, energy consumption, gross capital formation with economic growth: can lower financial openness change the curse into blessing // Resources Policy. 2021. №71(5). Pp.102013.

2. Cerdeiro D.A., Komaromi A. Financial openness and capital inflows to emerging markets: in search of robust evidence // International Review of Economics & Finance. 2021. №73(2).

3. Chinn M.D., Ito H. What matters for financial development? Capital controls, institutions, and interactions? // Journal of Development Economics. 2006. №81(1). Pp.163-192.

4. Montiel P., Reinhart C.M. Do capital controls and macroeconomic policies influence the volume and composition of capital flows? evidence from the 1990s // Journal of International Money & Finance. 1999. №18. Pp. 619-635.

5. Cottarelli, C., Giannini, C. Credibility Without Rules? Monetary Frameworks in the Post-Breton Woods Era // IMF, Occasional Paper.-1997.-№154.

6. Lane P.R., Milesi-Ferretti G.M. The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970-2004 // IMF Working Paper. 2006. № 06/69.

7. Quinn D., Schindler M., Toyoda A.M. Assessing measures of financial openness and integration // IMF Economic Review. 2011. № 59(3). Pp. 488-522.

8. Heathcote J., Perri F. Financial globalization and real regionalization // Journal of Economic Theory. 2004. № 119 (1). Pp. 207-243.

9. Carmignani F., Chowdhury A. The impact of financial openness on economic integration: evidence from the Europe and the Cis // Economics Faculty Research and Publications. 2006. №73. DOI: 10.1007/3-540-34264-8_11.

10. Rostow W.W., McKinnon R.I. Money and Capital in Economic Development // American Political Science Review. 1974. №68(4). Pp.1822.

11. Hartmann P., Maddaloni A., Manganelli S. The euro-area financial system: structure, integration, and policy initiatives // Oxford Review of Economic Policy. 2003. №19(1). Pp.180-213.

12. Ashraf B. N., Qian N., Shen Y.V. The impact of trade and financial openness on bank loan pricing: evidence from emerging economies // Emerging Markets Review. 2021. №47. Pp.100793.

13. Cerdeiro D.A., Komaromi A. Financial openness and capital inflows to emerging markets: in search of robust evidence//International Review of Economics & Finance. 2021. № 73(2).

14. Lan Faqin. Measurement of China's capital account opening // Journal of East China Normal University (SOCIAL SCIENCE EDITION). 2005. №37 (2). Pp. 87-94 (In Chinese).

15. Claessens, S., Glaessner, T. Internationalization of financial services in Asia // Social Science Electronic Publishing, 1998. DOI:10.1109/PIMRC.2006.254154

16. Mattoo A. Financial services and the WTO: Liberalization commitments of the developing and transition economies // The World Economy. 1999. №23(3). Pp. 351-386.

17. Luo, Y., Tanna, S., Vita, G.D. Financial openness, risk and bank efficiency: cross-country evidence // Journal of Financial Stability. 2016. Pp. 132-148.

18. Muller G. Troubled Relationships under the GATS: Tensions between Market Access (Article XVI), National Treatment (Article XVII), and Domestic Regulation (Article VI) // World Trade Review. 2017. №16(3). Pp. 449–474.

19. Wang W. On the Relationship Between Market Access and National Treatment Under the GATS // International Lawyer. 2012. №1045.

20. Tu Yonghong. RII--a new indicator to measure the real level of RMB internationalization // International Monetary Review. 2013 (In Chinese).

21. Jolliffe I.T., Cadima J. Principal component analysis: a review and recent developments // Philosophical Transactions of the Royal Society Mathematical Physical & Engineering Sciences. 2016.

Результаты процедуры рецензирования статьи

Рецензия скрыта по просьбе автора

Ссылка на эту статью

Просто выделите и скопируйте ссылку на эту статью в буфер обмена. Вы можете также

попробовать найти похожие

статьи

|

|